MathConsult was founded in 1996 by Prof. Heinz Engl as a research company developing mathematics-based solutions for the producing industry and for financial institutions.

Our projects come from various application fields:

- Iron and Steel

- Automotive industry

- Astronomy

- Electrical and magnetic engineering

- Medical Imaging

- Plastics Industry

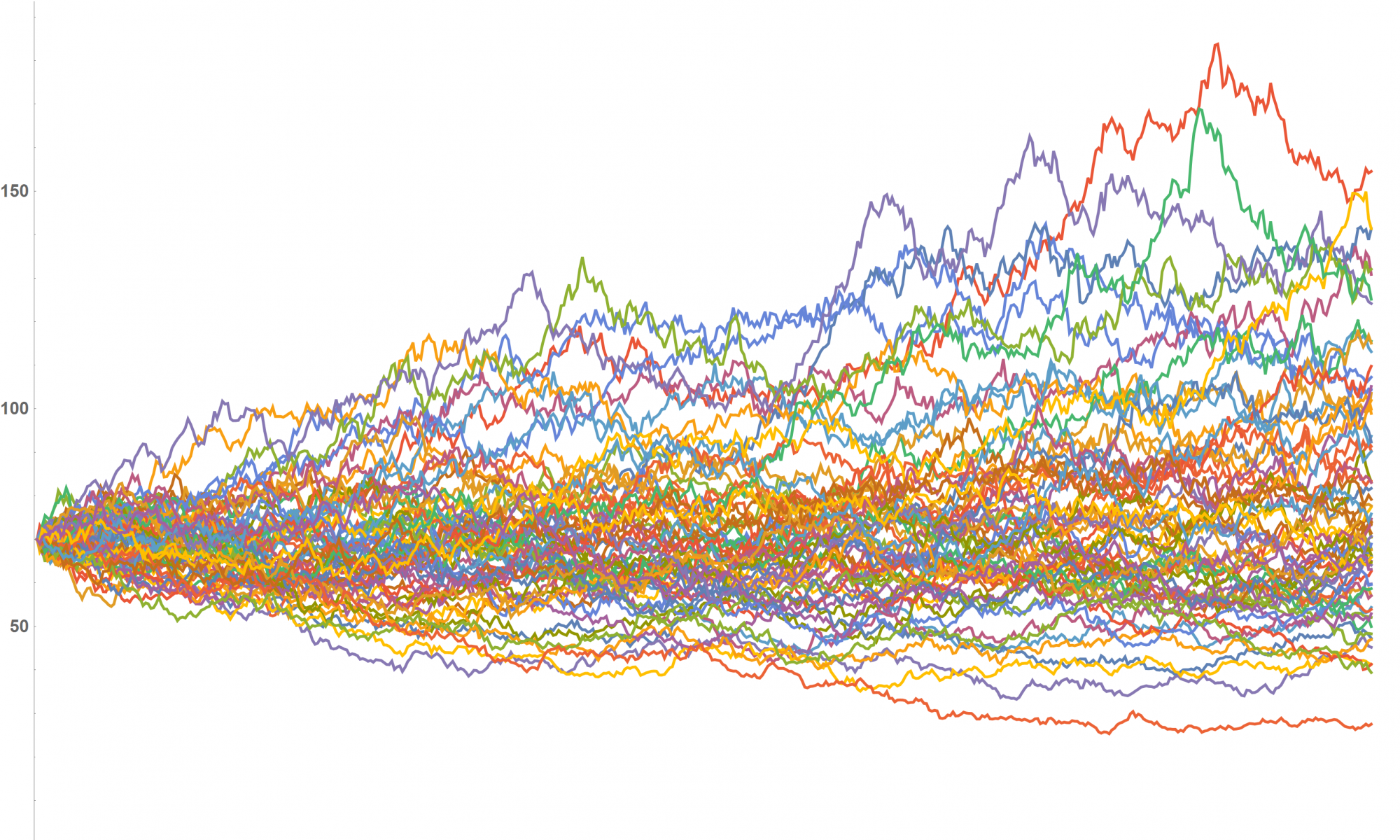

- Banking, asset management, insurance.

Our team consists of 25 scientists with a quantitative background: We have degrees in mathematics, physics and computer science. Almost 50 percent of us hold a Ph.D.

Cooperations and research output:

We have research cooperations with the Radon Institute for Computational and Applied Mathematics (RICAM) of the Austrian Academy of Sciences and with universities in Austria and from abroad.

For the last decade, MathConsult’s scientists have published more than 200 papers in journals and conference proceedings as well as a few books.

We have been awarded research grants from the European Union (within the Horizon 2020 framework), from the Austrian Forschungsförderungsgesellschaft and from the Upper Austrian government (within the OOE2020 framework).

MathConsult is headed by Dr. Andreas Binder.